📈

0.7%

Real GDP Growth

2025 full year · vs. 0.9% in 2024

Lowest in the regionA data-driven snapshot of Romania's macroeconomic outlook in a regional context — covering twin deficits, inflation, monetary policy, unemployment, and GDP growth. Full-year 2025 data.

By Ella Kállai, Co-founder · Consilium Policy Advisors Group · office@cpag.ro · www.cpag.ro

📈

0.7%

Real GDP Growth

2025 full year · vs. 0.9% in 2024

Lowest in the region🛒

9.6%

Inflation (CPI)

2025 · Jan 2026: 9.62% YoY

Highest in EU since Jan 2024👷

6.0%

Unemployment Rate

2025 · ↑ from 5.5% in 2024

Higher plateau🏛️

−7.6%

Consolidated Budget Deficit

2025 · ↓ from −8.7% in 2024

Larger correction than expected🌍

−8%

Current Account Deficit

2025 · ↓ from −8.5% in 2024

Twin deficit vulnerabilitySix thematic analyses — data from Eurostat, NBR, Ministry of Finance, INSSE, ECB, European Commission

Section 01

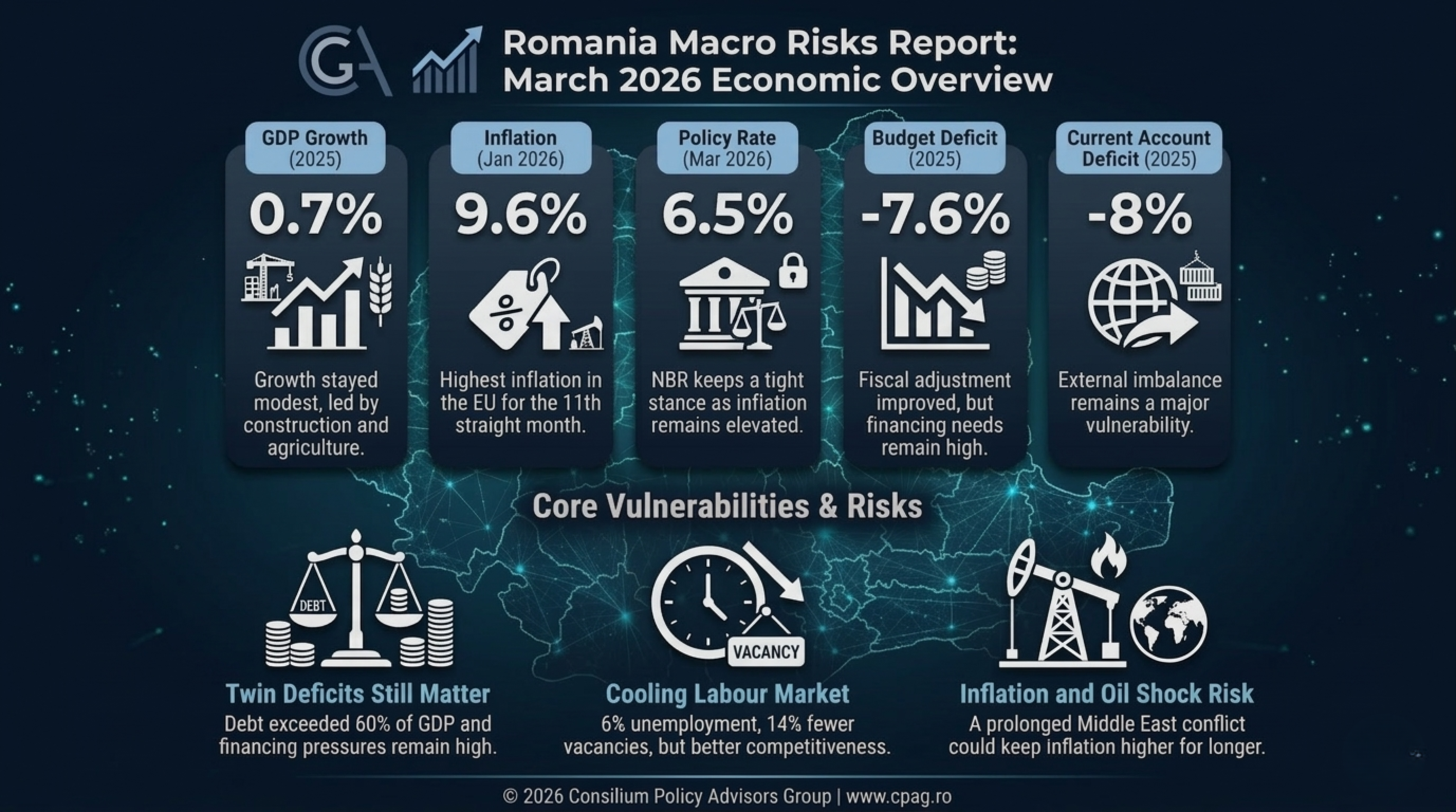

Macro Debriefing – March 2026

GDP expanded by only 0.7% in 2025 — below 2024's already modest pace. The twin deficit remains the fundamental weakness, though showing a larger-than-expected correction in H2 2025. Gross public debt exceeded the Maastricht threshold for the first time. High inflation expected to last until H2 2026.

Section 02

Larger correction than expected in H2 2025

The consolidated budget deficit was 7.6% of GDP in 2025 (down from 8.7% in 2024). Gross public debt exceeded the Maastricht threshold (60% of GDP) for the first time. Public financing need reached EUR 53bn in 2025. Government bond yields fell after markets acknowledged the H2 2025 correction.

Section 03

Annual inflation at 9.62% in January 2026

The combined effect of energy price cap lift in July and VAT rise from 19% to 21% in August pushed annual CPI to almost 10% YoY. Out of the 4pp increase in CPI since June, 64% was due to energy prices. NBR forecasts CPI at 3.9% by December 2026 and 2.9% by end-2027.

Section 04

Reference rate unchanged at 6.5%

NBR maintained the monetary policy rate at 6.5% pa (highest in EU, held since August 2024). Interest rate differential vs. ECB at 4.35pp. The REER with euro zone appreciated 3.9% vs. Dec 2024 and 14% vs. 2019. Euroisation of both loans and deposits continues to rise. No change expected at April 7, 2026 meeting.

Section 05

On a higher plateau · Wage inflation below CPI since July 2025

Average unemployment rose to 6% in 2025 from 5.5% in 2024. Vacancies declined 14% in 2025 vs. 2024. Labour market tightness declined — unemployed per vacant job increased from 13 (2024) to 16 (2025). Net wage growth slowed to 6.5% (12M avg, Dec 2025) from 13.4% (Dec 2024).

Section 06

Real annual GDP growth 0.7% in 2025

GDP grew 0.7% YoY in 2025 — lowest in the region. Supply drivers: agriculture and construction. Demand driver: gross fixed capital formation (+4.1% YoY). Net export drag improved significantly (-0.6pp in 2025 vs. -2.8pp in 2024). Labour productivity increased +3.8% while labour cost declined -0.3%.

Key upside and downside risks identified by the report for the year ahead

2025 full year · Romania vs. regional peers · Source: Eurostat

Labour Productivity

+3.8%

Labour productivity growth in Romania · 2025

Romanian labour productivity remains lower by 11% than in Poland, 14% than in Hungary, and 35% than in Czechia.

Labour Cost

−0.3%

Labour cost change in Romania · 2025

Romanian labour costs are lower by 15% than in Poland, by 34% than in Czechia, and at the same level as in Hungary.

Productivity per Labour Cost

Labour productivity per unit of labour cost — a measure of business profitability: