🏛️

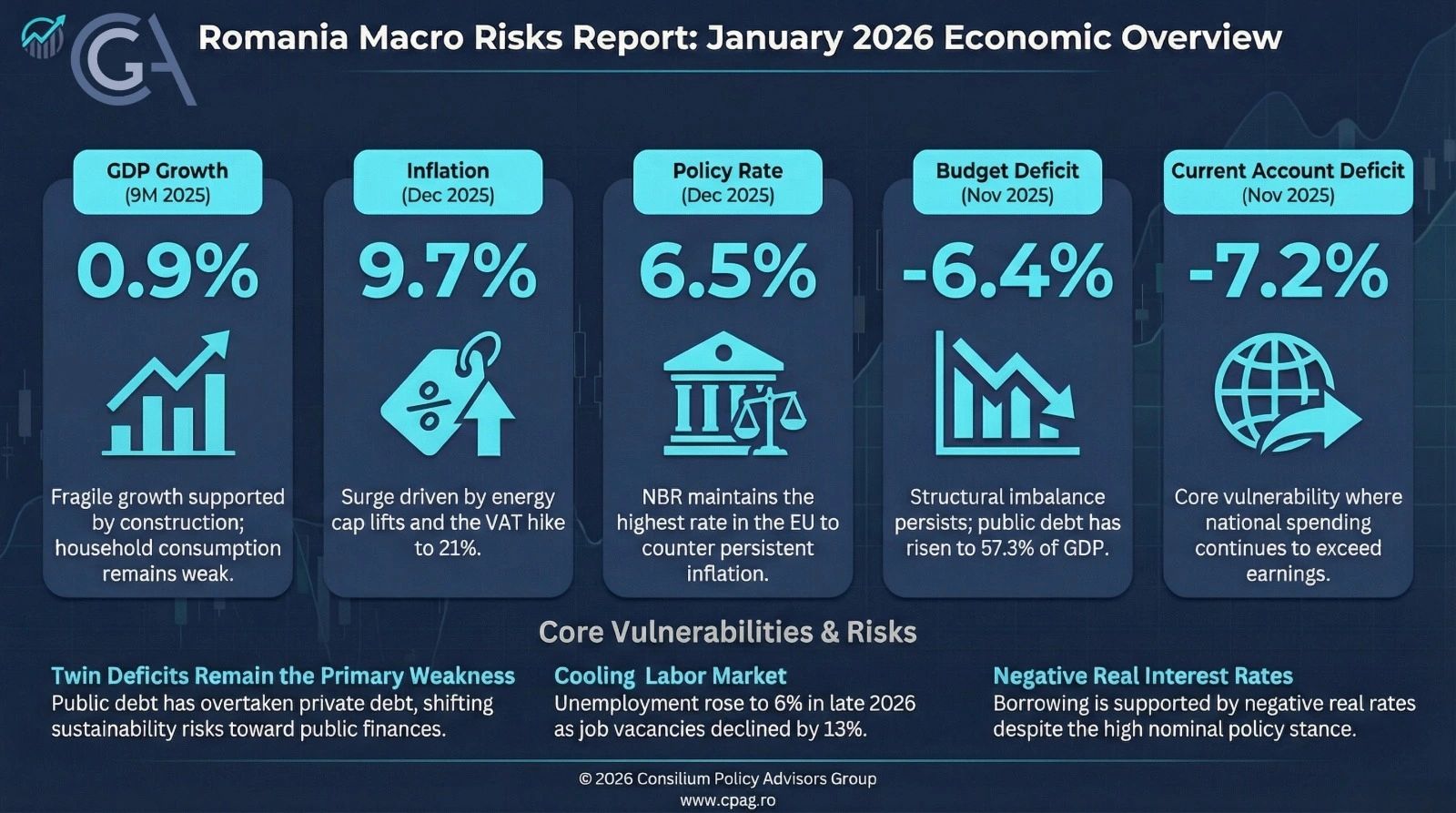

−6.4%

Consolidated Budget Deficit

11M 2025 · ↓ from −7.1% in 11M 2024

Beginning of correctionRomania's macroeconomic outlook under twin-deficit and inflation pressures

The January edition frames Romania's macro outlook through the interaction between fiscal adjustment constraints, inflation persistence, and the cost of external financing.

Author: Ella Viktoria Kállai

🏛️

−6.4%

Consolidated Budget Deficit

11M 2025 · ↓ from −7.1% in 11M 2024

Beginning of correction🌍

−7.2%

Current Account Deficit

11M 2025 · ↓ from −7.4% in 11M 2024

Twin deficit vulnerability🛒

9.7%

Inflation (CPI)

Dec 2025 · Annual avg. 7.3% in 2025

Highest in EU since Jan 2024🏦

6.5%

Monetary Policy Rate

Unchanged since August 2024

Highest in EU📈

+0.9%

Real GDP Growth

9M 2025 · vs. +1.1% in 9M 2024

Slowdown continuesFive thematic sections adapted for the macro report presentation.

Section 01

Beginning of the correction

Both the consolidated budget deficit and current account deficit narrowed slightly in 11M 2025, but remain among the largest in the EU. Gross public debt overtook private debt and continues rising.

Section 02

Annual inflation at 9.69% in December 2025

The CPI surge was largely policy-induced by energy price liberalisation and VAT changes in 2025. Disinflation is expected, but the path remains gradual and sensitive to external shocks.

Section 03

Reference rate unchanged at 6.5%

The NBR kept the policy rate unchanged amid weak growth and elevated inflation. Exchange-rate dynamics and increasing euroisation remain key transmission and confidence factors.

Section 04

Unemployment rising, vacancies declining

Labour market tightness softened in 2025, with weaker vacancy dynamics and slower wage momentum. Employment conditions remain exposed to demand and trade volatility.

Section 05

Real annual growth at 0.9% in 9M 2025

Growth remained fragile, with investment and selective external contributions acting as support. The overall trajectory stays below regional peers and vulnerable to policy and external shocks.

Key upside and downside risks identified for the year ahead.