The Window of Opportunity for Gradual Budget Deficit Adjustment Is Closing Fast

Although the urgency of reducing the budget deficit is universally acknowledged, the political will to achieve this goal appears increasingly paralyzed by the deadlock of reaching consensus within a four-party coalition whose members hold divergent economic views. Following the presidential elections, policymakers chose to quickly push through a package of tax hikes and then wait, hoping that economic momentum would spare them from the spending cuts that are actually needed — excessive expenditure growth being the primary driver behind the widening deficit. This approach to fiscal policy has now led us into yet another dead end.

By Laurian Lungu, Co-founder of Consilium Policy Advisors Group

Although the urgency of reducing the budget deficit is universally acknowledged, the political will to achieve this goal appears increasingly paralyzed by the deadlock of reaching consensus within a four-party coalition whose members hold divergent economic views. Following the presidential elections, policymakers chose to quickly push through a package of tax hikes and then wait, hoping that economic momentum would spare them from the spending cuts that are actually needed — excessive expenditure growth being the primary driver behind the widening deficit. This approach to fiscal policy has now led us into yet another dead end.

In early June, we published an article outlining a potential set of measures, including detailed projections through 2031 (https://cpag.ro/docs/Ajustare%20fiscala_Macro%20plan_04Jun25_EN.pdf). The principles were straightforward: indirect tax increases — which would have generated immediate budget revenues — necessarily paired with capping social contributions on other income categories, a 1 percentage point reduction in those contributions, and maintaining taxes on capital income such as dividends. Taken together, these measures were designed to protect consumption while, critically, also reducing public expenditure. It was a package grounded in economic logic rather than accounting mechanics, combining fiscal consolidation with partial support for consumption.

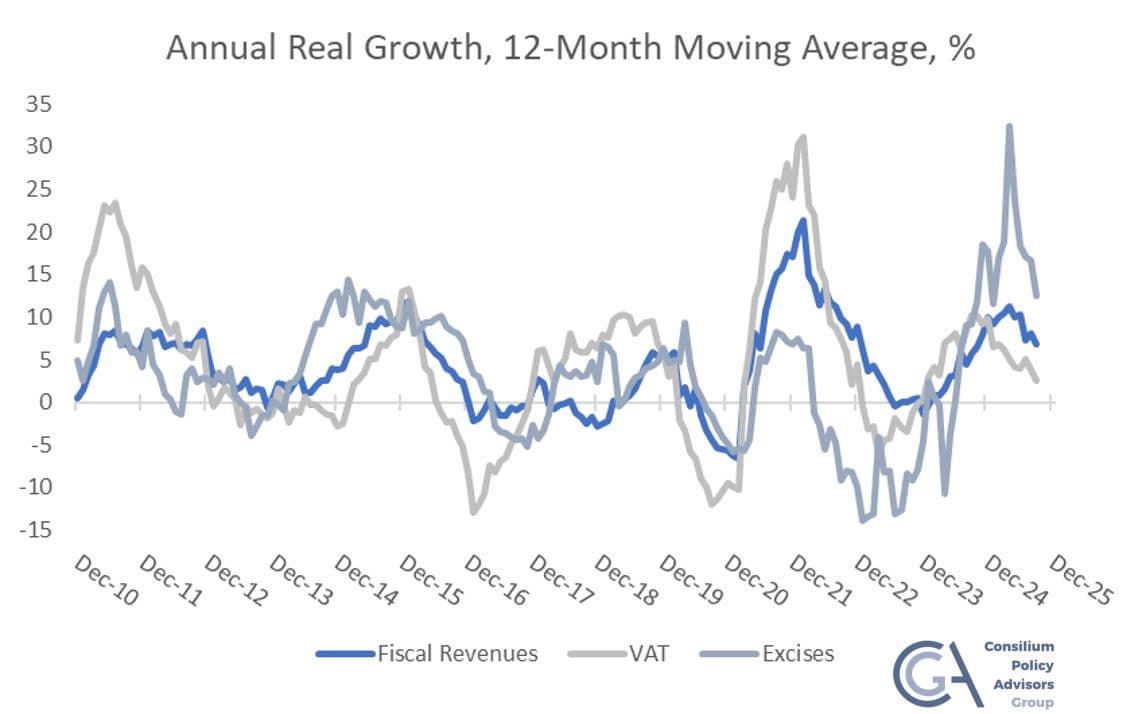

September's budget execution data reveals something unprecedented: despite the VAT and excise duty hikes introduced over the summer, revenues from these components — measured as a 12-month moving average — have declined in real terms. This stands in direct contrast to previous episodes, such as the VAT and super-excise increases of 2010 and 2014, which had a positive impact on revenues even in real terms, at least in the short run.

On a more positive note, VAT and excise revenues were still growing in September — up 2.6% and 12.5% respectively in real terms — though with a notably sharper deceleration compared to preceding months. What is becoming clear is that total fiscal revenues themselves are trending downward, falling from an annual real growth rate of 11.2% in April to 6.9% in September. While it is too early to draw firm conclusions, the continued deceleration in revenue growth is a worrying signal. It is highly likely that the marginal revenue impact of the new taxes coming into force at the start of 2026 will also prove smaller than currently anticipated.

Should this trend persist into the final months of the year, it should prompt an urgent rethink of the fiscal adjustment plan — specifically, by complementing existing measures with ones that actively support economic growth, namely those outlined above. A hike in dividend taxation can still be avoided. Exempting pension contributions under the second pillar and private pension schemes from social insurance contributions — which is economically unjustifiable — and capping contributions on other income categories would support consumption. Eliminating the turnover tax would help investment. All of these measures carry a very high cost-benefit ratio and, in essence, reduce future total budget revenues by dampening current economic activity. Given the present context, implementation in 2026 would be difficult, but discussions could begin now with a view to rolling them out in 2027.

Market signals suggest the Romanian economy is slowing, with the effect becoming more pronounced from September onwards. Recent growth forecasts for this year — 1% from the IMF and 0.6% from the National Prognosis Commission — appear overly optimistic in the current environment. These projections also feed into the deficit and growth forecasts for 2026, which were already going to be very difficult to meet. With inflation running at 10%, a policy of fully freezing certain budget expenditures in 2026 — essential to hitting the committed deficit target — will be harder to sustain against a backdrop of rising social tensions. Compounding this is the elevated risk of a potential negative shock from external markets, particularly capital markets. With debt and financing needs on an upward trajectory, the knock-on effects of such a shock would push Romania's financing costs sharply higher, further weakening its fiscal position.

In recent months, the authorities have rightly focused their efforts on avoiding the triggering of macroeconomic conditionality, which would have led to the suspension of EU funds next year. However, fiscal consolidation cannot be achieved without a significant reduction in spending over a relatively short timeframe, however difficult that may seem. The fiscal space for further tax increases has narrowed considerably, and early budget execution data suggest Romania may be approaching the peak of its Laffer curve — the point at which any additional tax increase actually reduces total budget revenues.

The time left to correct the trajectory of the budget deficit, as currently conceived, is shrinking by the day. The probability that Romania will consolidate its deficit through organic growth — thereby gradually bringing expenditure down from the estimated 44% of GDP this year — is diminishing. Romania needs economic growth, political stability, and economically coherent decision-making. Without these, the risk of a market-forced fiscal adjustment remains high, at least through the end of 2026.