Silver Prices and Their Implications for the Economy

Back in the 70's the wealthy Hunt brothers became convinced that inflation would destroy the dollar's value. This article explores silver's historical role and its current economic implications.

By Laurian Lungu, Co-founder of Consilium Policy Advisors Group

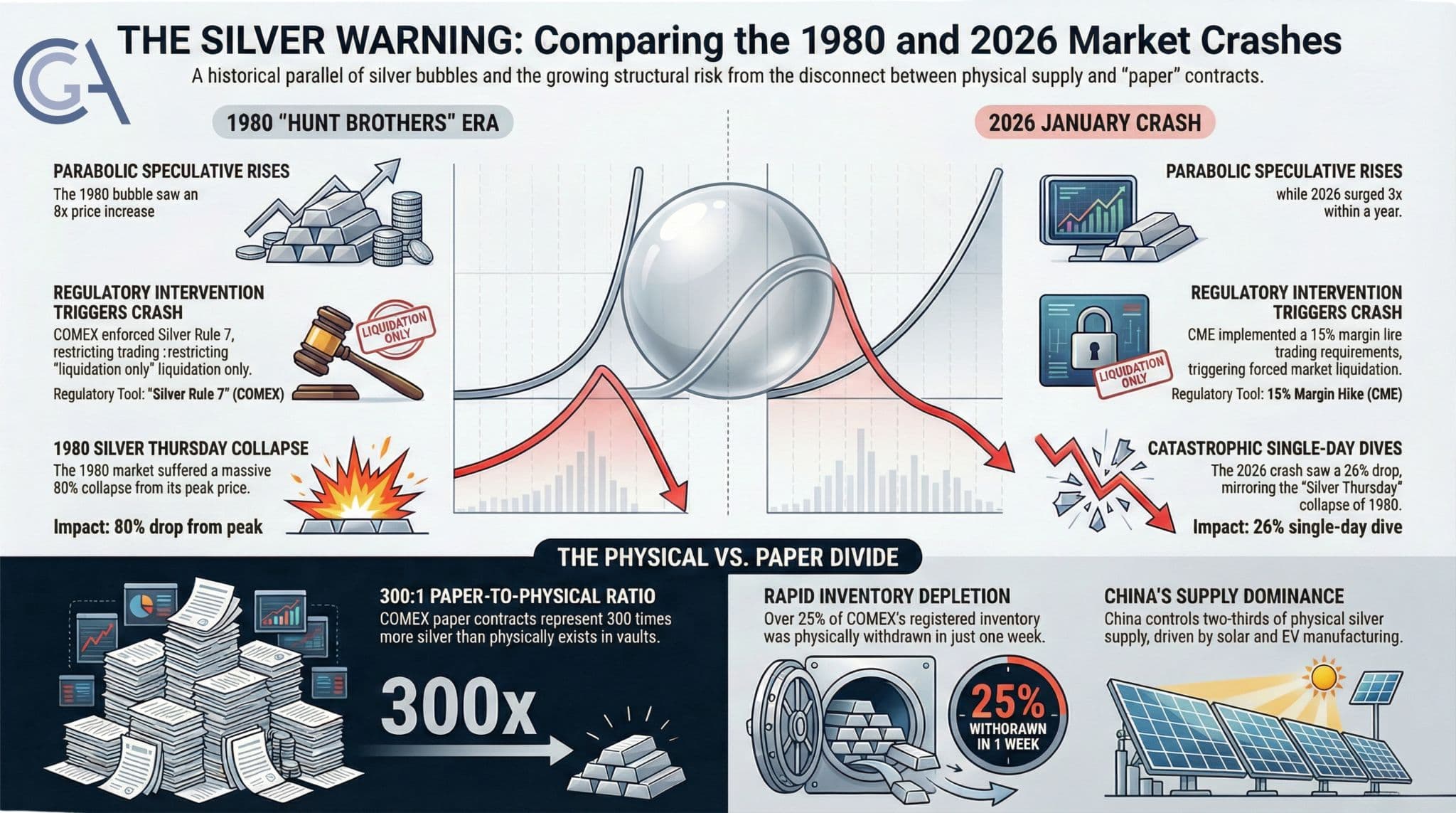

Back in the 70's the wealthy Hunt brothers became convinced that inflation would destroy the dollar's value. At the time U.S. citizens were prohibited from owning gold, so the Hunt brothers chose silver, then standing at USD 1.50/ounce, as their speculative hedge. They decided to protect their wealth by cornering the silver market. Silver went from around USD 6/ounce in early 1979 to a peak of USD 50/ounce in January 1980, an 8 times increase in about a year. Eventually, the Hunts owned the equivalent of about 70% of the world silver. On January 1980, the Commodity Exchange Inc. (COMEX) introduced "Silver Rule 7" to end the speculation, imposing strict restrictions on purchases on margin and eventually "liquidation only" trading. This triggered a price crash on "Silver Thursday" March 27, 1980 when silver fell by 50% to USD 10/ounce, down 80% from its peak reached just two months earlier. In the wake of Silver Thursday, many of the banks and trading firms that had loaned the Hunts money also found themselves in financial trouble, resulting in a secondary wave of bankruptcies and mergers. The Federal Reserve (FED) was forced to intervene to allow for an orderly liquidation of silver positions.

Lessons from the history are always useful. The recent 26% single day dive in silver prices at the end of January 2026 bears striking parallels to the 1980's episode. There was a parabolic silver price rise driven by speculation — Hunt Brothers' 8 times vs. 2026's 3 times in a year — supported by leveraged speculators, which were unable to meet margin calls, triggering a "liquidation only" dynamics, with forced selling and no new buyers. There was a catastrophic single-day crash when the leverage unwound.

What triggered the adjustment was the exchange intervention through margin requirement changes (margins are deposits needed to be kept as collateral at all times to cover potential losses). The Chicago Mercantile Exchange (CME) moved to a percentage-based margin system in January 2026, hiking maintenance margins to 15% for standard positions, in fact continuing a process of raising margin requirements initiated in September last year. The mechanism was similar to the "Silver Rule 7" in the 80's. The Shanghai Futures Exchange also raised margin requirements albeit at a smaller pace. The standard lesson here is that the exchanges have the power to end speculative bubbles by changing the rules mid-game. When they hike margins on a leveraged market, they can force a liquidation cascade that becomes self-reinforcing. That's exactly what happened in 1980, and it is what happened again in January 2026.

Another lesson is that globalisation comes with risks if regulatory standards differ. In China there is a speculation frenzy and Chinese investors had been piling into precious metals with platforms, some unregulated, offering 40-times leverage — which means that requiring margin was equal to as little as one-fortieth of the spot price. The leverage has an inverse relationship with the margin requirement. It was no surprise that silver gained 60% in just four weeks there as a raft of other commodities, including gold and palladium, together with bitcoin, were used as investing assets.

China controls around two thirds of global physical silver supply being the largest consumer of silver for solar PV modules, electronics, and electric vehicles. Before the crush, physical silver in Shanghai was trading at a substantial premium to paper contracts. In theory the arbitrage should have been simple: one could buy silver on COMEX, ship it to Shanghai, and collect the profit by deducting shipping costs. But in reality, it stopped working because there was not enough silver to move. COMEX, as all other exchanges, operates on a fractional reserve system. The number of paper silver contracts outstanding represents roughly 300 times more silver than physically exists in COMEX vault. Given its demand, and as a response to global trade frictions, China imposed export licensing requirements at the beginning of 2026. The arbitrage opportunity given by the paper-physical spread has been extraordinary and historically unprecedented. Between early and mid-January, in just a week, more than a quarter of COMEX's registered inventory disappeared, being physically withdrawn for delivery from COMEX. Silver inventories on the Shanghai Futures Exchange (SHFE) have also plunged to their lowest levels in nearly a decade, underscoring the growing tightness in the global physical silver market.

At the moment the silver market is still in a self-correcting mode. The January 2026 crash eliminated overleveraged speculators and the chances are that markets where physical demand is stronger, like China, will gradually build out an alternative price discovery system. If enough of the physical market migrates to London, Shanghai, Dubai, and other delivery markets, COMEX contracts might become less relevant for the actual metal. On the other hand, demand for silver from companies who need it as an input could drop as alternative sources are used to replace silver.

Gold has also risen strongly over the last months, largely due to geopolitical uncertainty and fears that a bubble is forming in some stock markets. But gold has deeper physical markets, which makes it easier to absorb shocks, is used on a much smaller scale as an industrial component — with price being a major impediment — and faces a more stable demand from large institutions such as central banks. The average gold-silver price ratio stood at around 70 between 2005 and the present day. Currently it is at around 60. One question is of course, whether the current growth rates in commodity prices, notably silver and gold, can be maintained and for how long.

The 2026 crash is a warning shot. The question is whether regulators act before a delivery failure from one exchange occurs or whether they wait for the system to get to a difficult position and then impose emergency rules, like in the 80's. Time will tell.